Premature Warrant

By Atty. Irwin C. Nidea Jr.

"When WDL is issued, it has far-reaching implications as far as taxpayer remedy is concerned. It is only the Court of Tax Appeals (CTA) that can stop its execution. No appeal taken to the CTA from the decision of the Commissioner of Internal Revenue on a disputed assessment shall suspend the payment, levy, distraint, and/or sale of any property of the taxpayer for the satisfaction of his tax liability, unless the CTA suspends the collection after payment of bond."

Since businesses are struggling with the prolonged pandemic, the BIR has no source of revenue. There is no income tax nor value added tax collection since there are no sales of goods and services during lockdown. However, the government cannot stop operating specially during this difficult time as many families also depend on it for financial aid. The BIR is pressured to look for funds on the fly. As expected, it is now targeting tax assessments that are ripe for the picking.

Unfortunately, there are cases when warrants of distraint (WDL) and levy/garnishment are prematurely issued. When is the issuance of WDL premature? Can the BIR issue WDL and instigate enforcement proceedings when the assessment process is still in the Final Assessment Notice (FAN) or Final Decision on Disputed Assessment (FDDA) stage?

Under Revenue Memorandum 39-2007, revenue officers are instructed to start enforcement proceedings in the following instances:

Under Revenue Memorandum 39-2007, revenue officers are instructed to start enforcement proceedings in the following instances:

1. Disputed assessments finally decided by the Commissioner or Regional Director, as the case may be, against the taxpayer;

2. Assessments upheld by the CTA in Division whether or not appealed to the CTA En Banc, or upheld by the CTA En Banc whether or not appealed to the Supreme Court. Based on this RMO, upon issuance by the Commissioner or Regional Director of the final decision on the disputed assessment (FDDA) against the taxpayer or upon issuance by the CTA in Division or En Banc of its decision upholding the assessment, Warrants of Distraint and Garnishment, and/or Levy shall be immediately issued and served. This was reiterated in RMO No. 42-2010.

So, the BIR may enforce collection proceedings only when the Commissioner or the Regional Director has issued the FDDA or when the CTA has promulgated a decision. The BIR need not wait for the assessment to become final and executory.

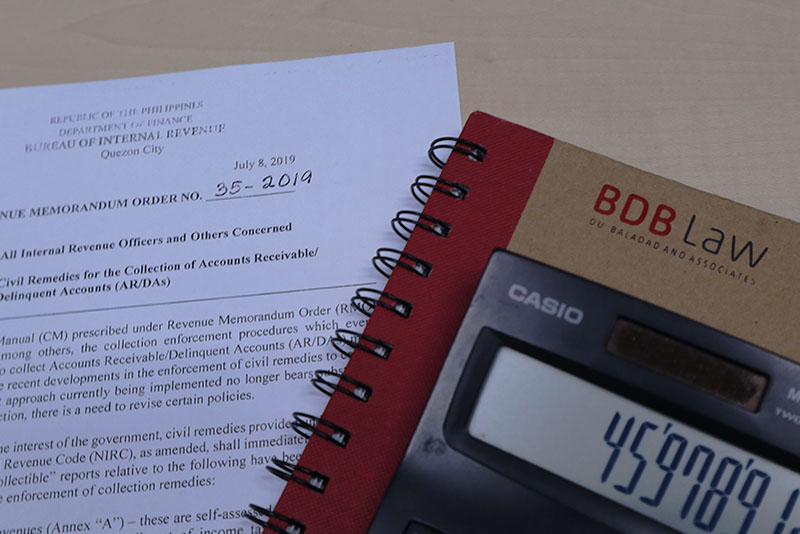

These RMOs however were superseded by RMO No. 35-2019. Now, collection cannot be pursued just because the Commissioner or Regional Director has issued a final decision of disputed assessment. WDL can only be issued in the following instances:

1. Unpaid Revenues - these are self-assessed taxes arising from dishonored check, unpaid second installment of income tax due of individual taxpayers and duly validated unpaid tar due per tax returns; and

2. List of Unpaid Tax Assessments: (1) Unprotested Final Assessment Notice; (2) Unappealed FDDA; (3) Unappealed Decision of the Commissioner; and (4) Final and Executory Decision by the Court - these are tax assessments arising from investigation which have become ''final and executory".

Clearly, revenue officers are only authorized to issue WDL when an assessment is “unappealed” or the decision of the CTA becomes “final and executory”. They cannot enforce collection when the assessment is still under protest or is still being appealed at the CTA. RMOs 39-2007 and 42-2010 are no longer controlling. Revenue officers must observe the guidelines of RMO 35-2019 which defines what are considered “unappealed” or “final and executory” assessments that can be subjected to enforcement proceedings.

When WDL is issued, it has far-reaching implications as far as taxpayer remedy is concerned. It is only the Court of Tax Appeals (CTA) that can stop its execution. No appeal taken to the CTA from the decision of the Commissioner of Internal Revenue on a disputed assessment shall suspend the payment, levy, distraint, and/or sale of any property of the taxpayer for the satisfaction of his tax liability, unless the CTA suspends the collection after payment of bond. So, a taxpayer has no choice but to spend for litigation if he wants to protect his interest.

It is important that revenue officers restrain themselves from issuing untimely WDLs. They will not only trample upon taxpayer’s right to due process, but they might also jeopardize the collection efforts of the government. It is understandable that revenue officers need to reach their collection targets. But they must take note that when taxpayer’s rights are violated, the assessment and collection process of the BIR will be declared void by the courts. If this happens, the government will fall on its own sword, with an empty purse.

The author is a senior partner of Du-Baladad and Associates Law Offices, a member-firm of WTS Global.

The article is for general information only and is not intended, nor should be construed as a substitute for tax, legal or financial advice on any specific matter. Applicability of this article to any actual or particular tax or legal issue should be supported therefore by a professional study or advice. If you have any comments or questions concerning the article, you may e-mail the author at This email address is being protected from spambots. You need JavaScript enabled to view it. or call 8403-2001 local 330.